Bank Manager Calls Black Teen’s Mom “Nobody” — Then She Fires the Branch Manager With One Call

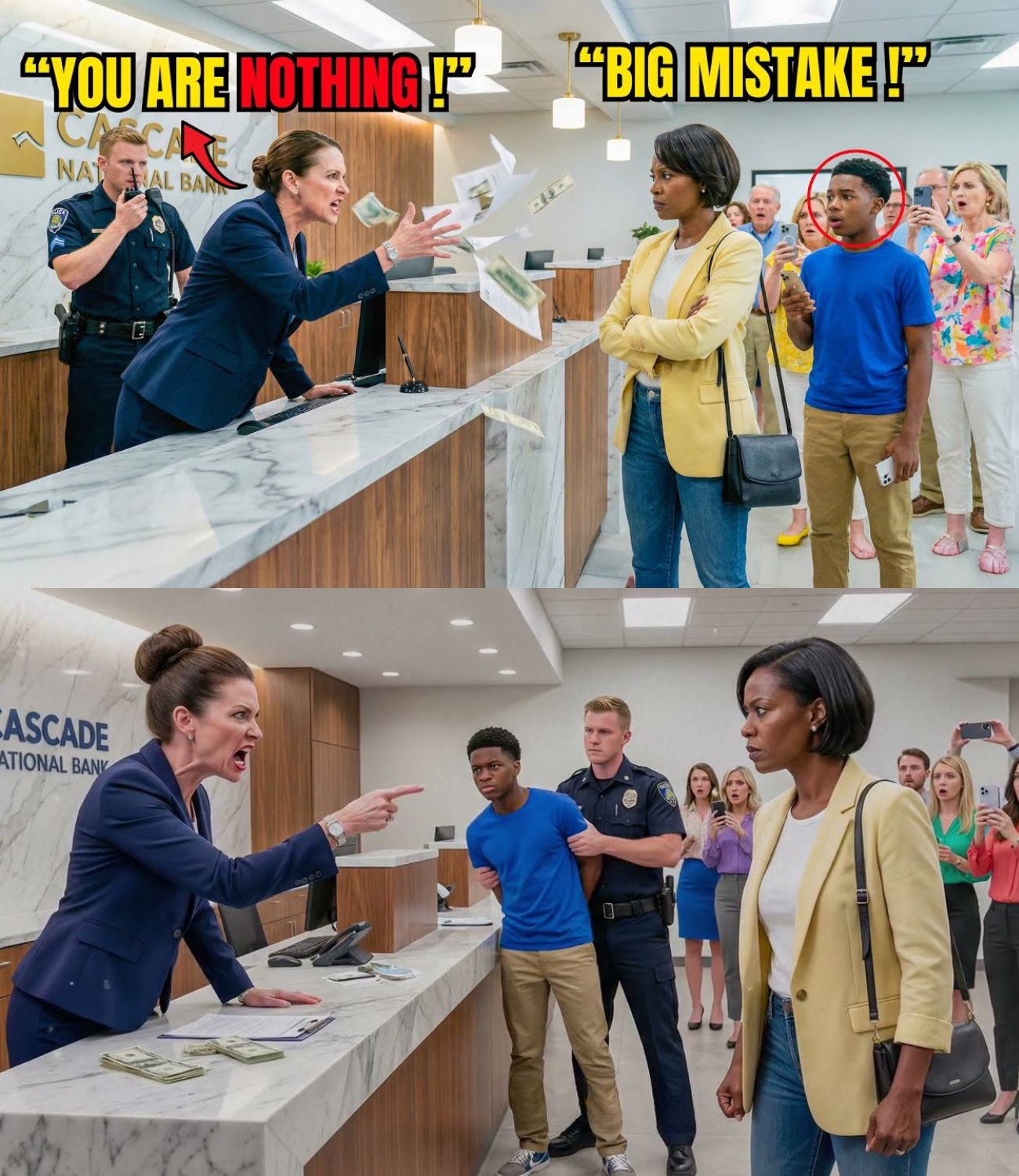

$500 from a 16-year-old. Diane Whitmore’s voice cuts across the bank lobby. Where did you people really get this money? She’s standing now, arms crossed, looking down at Jamal Carter like he’s something she stepped in. Ma’am, it’s from my summer job and birthday money. Don’t ma’am me. I’ve been doing this for 6 years.

I know it’s suspicious when I see it. She taps her manicured nails on the desk. This bank serves established clients, people with real credentials, real money, not whatever this is. Regina Carter, Jamal’s mother, speaks quietly. We provided every document you asked for. Documents can be faked. Diane leans back in her chair, a tight smile on her lips. Let me be clear.

People like you don’t belong in a bank like this. You’re nobody. Maybe try somewhere more appropriate. The lobby goes silent. Other customers stare. Regina’s face doesn’t change, but her hand resting on her phone moves slightly. Have you ever watched someone destroy their entire career without knowing it? 45 minutes earlier, Regina Carter pulls into the Cascade National Bank parking lot in a 2018 Honda Accord.

Not luxury, not new, just a regular car with a few scratches and a high school sticker on the bumper. Jamal sits in the passenger seat. Mom, there’s a branch closer to home. This one’s fine. Regina checks her reflection. Jeans, navy blazer, small silver earrings, a worn leather purse. Everything about her is ordinary, middle class, forgettable.

That’s the point. Inside the lobby whispers prestige, marble floors, high ceilings, classical music. Behind bulletproof glass, tellers help customers. A white couple in their 60s sits with a loan officer laughing. They wear Patagonia and pearls. They look like they belong. At reception, a young man smiles. His name tag reads Kevin.

Good morning. How can I help you? We’re here to open a student checking account. Kevin types, then waves towards someone. Miss Whitmore, could you help the Carters? Diane Whitmore emerges from a glasswalled office. 48. Blonde hair pulled tight. Expensive suit. She carries a mug that says world’s best manager.

Her eyes land on Regina and Jamal. Something shifts in her expression. a tightening around her mouth, a pause before she smiles. Regina catches it. Right this way. Diane’s office has glass walls. Everyone in the lobby can see inside. On her desk, family photos in silver frames, two blonde kids skiing.

Behind her, framed certificates. Branch manager of the quarter. Excellence in customer service. Leadership achievement award. The irony will land harder later. Diane settles into her chair. So, students account for Jamal. I got a summer job at Rosewood Community Center. Community Center. That’s nice. Diane types slowly. I’ll need IDs, social security numbers, proof of address.

Regina provides everything. Driver’s license, utility bill, Jamal’s student ID from Jesuit high school. Diane examines the utility bill longer than necessary. Her eyebrow lifts. This address, Southeast Alama Ridge, that’s an expensive neighborhood. Do you rent or own? First test. We own. Diane sets it down.

And what do you do for work, Miss Carter? I work in healthcare. Diane’s face softens into something like sympathy. Oh, a nurse. That’s wonderful. Steady work. Hard work, I’m sure. Regina doesn’t correct her. Just nod. Second test. Diane assumed, made a judgment, and Regina deliberately lets her because Regina didn’t come here just to open an account.

She came to see how her bank treats people without obvious wealth. So far, not good. And the initial deposit amount, $500, Jamal says. Dian’s fingers pause. 500 is more than she expected. That’s quite a bit for a summer job. Some of it’s birthday money from my grandparents. Birthday money? I see. Diane stops typing.

She’s studying them now. Where does a 16-year-old get $500? Not curiosity, accusation. Regina’s fingers tap once on her armrest. Just once. She’s deciding whether to speak up now or let this play out. Outside the glass, a young white couple in athletic wear approaches another banker, Nike Lululemon. The banker greets them warmly, smiling.

No questions about their money, no suspicious looks. 8 minutes later, they walk out with their new account. Inside Diane’s office, the Carters have been sitting for 17 minutes. They haven’t even started the paperwork yet. Diane leans forward. I’m going to need documentation for these funds, a letter from your employer verifying the paycheck, and for the birthday money, perhaps a list of relatives who gave gifts.

This isn’t standard procedure. It’s targeted. Jamal’s voice rises slightly. Are you serious? Diane’s eyes narrow. Young man, I’m trying to help you. If you have an attitude, I can decline this application altogether. Banking is a privilege. Regina places a hand on Jamal’s shoulder. Ms.

Whitmore, we’ve provided every standard document. You’re now requesting things not on your checklist. Why? Diane sits back defensive. I have discretion to request verification when necessary. And frankly, your attitude isn’t helping. A teller outside, an older black woman named Ms. Patterson, has stopped her work. She’s watching through the glass.

Her face is tight with recognition. She’s seen this before. Regina pulls out her phone. Bank policy prohibits recording, Diane says sharply. I’m not recording. Regina types something quickly. A text message to someone. Just checking consumer protection guidelines. Who did she text? What did she say? That answer is coming.

Diane Whitmore refreshes her computer screen. There’s an issue with your credit authorization form, Miss Carter. You didn’t initial box 3B. Regina leans forward to look. I initialized every box. That’s my signature right there. Diane shakes her head, already sliding a fresh form across the desk. This one has red pen marks indicating missing information.

The system shows it’s incomplete. You’ll need to fill out a new one. Federal regulations, I’m afraid. Regina examines both forms. They’re identical. What specifically is missing? Box 3B. Like I said, Dian’s tone sharpens. I understand this might be confusing, but these are compliance requirements. Confusing? The word hangs in the air like an insult.

Jamal whispers, “Mom, can we just do it?” Regina shakes her head slightly. She recognizes what’s happening. She’s been here before in different contexts. The excessive scrutiny, the manufactured obstacles, the assumption that she won’t understand the rules. She fills out the second form anyway. initials every single box with exaggerated clarity. Slides it back.

Diane scrutinizes it like she’s examining a counterfeit bill. Holds it up to the light. Checks the signature three times. Through the glass walls, another scene unfolds. A white couple in their 30s approaches a different banker’s desk. The woman has her hair in a messy bun. The man wears a faded college sweatshirt.

They’re opening a joint account. The banker is smiling, joking with them. No one asks to see their utility bill twice. No one questions their address. No one demands extra documentation. 7 minutes later, they’re done. They walk out holding hands, laughing about something. Back in Dian’s office, 23 minutes have passed. Diane sets the form down.

Now about $500. I’m going to need verification. A letter from the Rosewood Community Center on official letterhead stating Jamal’s hourly wage and total earnings to date for a checking account. Regina’s voice stays level, but there’s steel underneath. That’s not standard procedure. It is when I deem it necessary.

Diane folds her hands on her desk. And for the birthday money, I’ll need a sworn statement from the relatives who gave it. names, addresses, amounts, and their relationship to Jamal. Jamal stares at her. You want my grandparents to write a statement about birthday money? Bank secrecy act requirements. We have to verify the source of all funds.

Dian’s smile is thin and sharp. Surely you understand. We can’t just accept cash without knowing where it came from. Regina’s jaw tightens. The Bank Secrecy Act applies to transactions over $10,000. My son is depositing $500. For a moment, Dian’s mask slips. She didn’t expect Regina to know that. I have discretionary authority, she says quickly. And I’m exercising it.

If you can’t provide the documentation, I can’t open the account. Can’t or won’t? Diane stands up. the power move of someone who’s lost the argument and needs to physically assert dominance. Miss Carter, I don’t appreciate your tone. I’m trying to protect this institution from fraud. Fraud? Regina says the word slowly.

You think my 16-year-old son is committing fraud with his community center paycheck. I think there are patterns we’re trained to recognize. Diane crosses her arms. Red flags. And frankly, this situation has several. What patterns? Regina stands too, matching her. What red flags? Be specific. The glass walls mean everyone can see this now.

Kevin at reception has stopped greeting customers. Ms. Patterson at the teller window has abandoned her transaction entirely. A man in a suit near the ATM is openly staring. Dian’s face flushes. She’s aware of the audience. It makes her more aggressive, not less. High value deposits from minors, vague employment claims, reluctance to provide standard documentation.

She counts on her fingers. And your attitude, Miss Carter, is not helping your son’s case. My attitude? Regina speaks loud enough for others to hear. I’ve provided every document on your account opening checklist. You’ve requested additional items that aren’t policy, and now you’re calling my compliance attitude. I’m calling your hostility attitude.

There’s a difference between a customer and someone looking to cause problems. Jamal’s voice cracks. We’re not trying to cause problems. I just want to deposit my paycheck. Diane barely glances at him. Then perhaps your mother should let me do my job instead of questioning every procedure. Regina pulls out her phone again.

I said no recording. Dian’s voice rises. I’m not recording. I’m documenting. Regina types quickly. Another text message sent to someone who matters. Diane sees red. That’s it. I’m not comfortable proceeding with this application. I think you should leave. Leave. Regina doesn’t move. You’re refusing service.

I’m exercising my right to decline an account when I have concerns about the legitimacy of the customer relationship. legitimacy of the customer relationship. Regina repeats it slowly, letting each word land. What concerns specifically do you have about our legitimacy? Diane opens the glass door of her office. A clear dismissal.

I don’t need to explain every operational decision to you. This conversation is over. No, it isn’t. Regina stays seated because you’re going to tell me in front of all these witnesses exactly what concerns you have about my family. The lobby has gone completely quiet. Eight customers are watching now. Three tellers, Kevin.

A security guard near the entrance has started walking toward them. Dian’s hands are shaking from anger or fear. It’s hard to tell. Fine. You want specifics? Your son shows up with $500 in cash. You live in a neighborhood you clearly can’t afford. You claim to work in healthcare, but you’re dressed like She stops herself almost.

Like what? Regina’s voice is dangerously soft. Like someone who doesn’t belong in a private bank. The words come out in a rush. This isn’t a community bank. We serve established clients with verified income and assets. People who contribute to the economy, not not what. Diane has gone too far to stop. The audience, the pressure, the loss of control. It all crashes together.

Not people like you. Her voice echoes off the marble. People who come in here with demands and attitudes and expect us to just ignore every protocol because you’ll cry discrimination if we don’t. Well, I’ve been managing this branch for 6 years, and I know who belongs in a bank like this. She steps closer, looking down at Regina and Jamal.

You want the truth? Fine. I have concerns about the source of your funds. I have concerns about your financial situation. I have concerns about whether you even understand how banking works. And yes, I’m refusing service because this is my branch and I decide who opens accounts here. Her voice drops to something cold and final.

People like you always play the victim. You come in expecting special treatment. And when we follow policy, you make it about race. Well, it’s not. It’s about standards, professional standards. This bank has a reputation to maintain. And frankly, Miss Carter, she looks Regina up and down with pure contempt.

You’re nobody. You don’t belong here. This isn’t some welfare office where you can walk in off the street. We serve successful people, real professionals. Maybe try a community credit union somewhere more appropriate for your needs. The silence that follows is absolute. Someone in the lobby gasps audibly. Ms.

Patterson at the teller window has her hand over her mouth. Kevin looks like he might be sick. The security guard, Marcus Thompson, has stopped walking. He’s a 52-year-old black man, retired police officer. He knows exactly what he just heard. Jamal’s eyes fill with tears. He blinks them back hard, but not before one escapes.

His mother just got called nobody in public. He just got accused of being a criminal, and there’s nothing he can do about it. Regina’s expression doesn’t change, but something behind her eyes does. She’s not angry anymore. She’s resolved. Her phone, still in her hand, shows a text message sent 3 minutes ago. Timestamp 11:02 a.m. The recipient isn’t visible from where Diane stands, but the message is simple.

Discrimination incident. Downtown branch. Diane Whitmore. Stand by. Regina looks at Diane Whitmore for a long moment. Then she speaks, her voice carrying through the silent lobby. You’re absolutely sure about that? That I’m nobody? That I don’t belong here? Diane, emboldened by her own momentum, lifts her chin. Completely sure.

Good. Regina’s voice is ice. I wanted to be certain before I made the call. She lifts her phone to her ear and Diane Whitmore’s world begins to end. Regina presses a number on her phone. It rings once, twice. Diane crosses her arms, confident. Who are you calling? Your lawyer. Good luck with that. The call connects.

Regina taps the speaker button. Her voice is professional, cold, controlled. Janet, this is Regina. A woman’s voice comes through crisp and immediate. Dr. Carter, I got your text. What happened? Dr. Carter. Dian’s smile falters. Regina speaks slowly, clearly, loud enough for the entire lobby to hear. I’m at our downtown Portland branch with my son.

We came to open a student checking account. The branch manager, Diane Whitmore, refused service. She questioned the legitimacy of my son’s $500 deposit from his summer job. She demanded non-standard documentation not required by bank policy. She accused us of fraud. Dian’s face goes pale. When I asked for an explanation, she told me that people like me don’t belong in this bank, that we should try somewhere more appropriate, that I’m nobody.

Regina pauses. She said this in front of approximately 15 witnesses, including bank employees and customers. Several are recording on their phones. The voice on the other end, Janet Woo, chief human resources officer of First Western Financial Holdings, responds immediately. Is Miss Whitmore present? She is.

She’s listening. Diane Whitmore. Janet’s voice drops 20°. Do not move. Do not speak to anyone. Do not leave that building. Diane reaches for her desk, steadying herself. Dr. Carter, Janet continues, her tone shifting back to professional concern. I cannot apologize enough. This is a catastrophic failure of everything we stand for.

I’m sending the suspension notice now. Regional director Brooks is on route. He’ll be there in 6 minutes. Thank you, Janet. Regina ends the call. The lobby is dead silent. Every eye is on Diane. Diane’s mouth opens, closes. Dr. Carter, you’re Who are you? Before Regina can answer, Diane’s computer chimes. A new email notification.

Her hands shake as she clicks it open. From Janet Woo, chief human resources officer, First Western Financial Holdings to Diane Whitmore, CC Robert Brooks, Regional Director, Legal Department. Subject: immediate suspension. CEO directive. Miss Whitmore, you are hereby suspended without pay.

Effective immediately by direct order of CEO Dr. Regina Carter. Cease all work activities. Surrender your access badge, office keys, and all company property. Security has been notified and will escort you from the premises within 15 minutes. A formal investigation will commence Monday morning. You are prohibited from contacting any employees, customers, or representatives of First Western Financial Holdings regarding this incident.

Failure to comply will result in immediate termination and potential legal action. Janet Woo, Chief Human Resources Officer, First Western Financial Holdings. Diane reads it once, twice. Her face drains of all color. CEO. Her voice is barely a whisper. You’re the CEO. Regina stands. She’s not tall, but right now she seems to fill the entire room.

I’m Regina Carter, founder and chief executive officer of First Western Financial Holdings, the company that owns Cascade National Bank and 49 other branches across six states. Her voice is quiet, but it cuts like a blade. I built this company from a single branch 12 years ago. I sit on the board of three Fortune 500 companies.

I oversee $8 billion in assets. She steps closer. And you just told me I’m nobody. Diane sinks into her chair. Her hands are trembling so badly she can barely grip the armrests. I didn’t. I didn’t know. You didn’t say. If I had known who you were. If you had known, you would have treated us differently. Regina’s voice is steel.

That’s exactly the problem. Respect shouldn’t depend on knowing someone’s title. Marcus, the security guard, appears in the doorway. He’s been standing nearby, listening to everything. He looks at Diane without sympathy. Ms. Whitmore, I need your badge, keys, and company phone. Diane is crying now, mascara running. Please, I have kids.

I have a mortgage. I need this job. I didn’t mean you meant every word. Regina doesn’t raise her voice. She doesn’t need to. You said people like me don’t belong here. You called my son a fraud. You told me to find somewhere more appropriate in front of your employees, in front of customers, in front of my son. She glances at Jamal, who’s standing now watching his mother inhabit her full power for the first time in his life.

You meant it, Regina continues. And now you’ll face the consequences. Miss Patterson, the teller who’s been watching everything, approaches the office. Dr. Carter, I’m Evelyn Patterson. I’ve worked here for 11 years. I need to tell you this isn’t the first time I’ve seen her do this to other customers. I reported it twice. Nothing happened.

Regina pulls out her phone, opens her notes app. M. Patterson, would you be willing to provide a formal statement, dates, names, specific incidents? Absolutely. Kevin from reception joins them. I documented everything and emailed HR 30 minutes ago. Timestamps, witness names, everything. Another teller, a young Latino man named Carlos.

I saw her do this to a black couple last month. Same questions about their money, same attitude. The evidence is piling up. This isn’t one incident. It’s a pattern. Diane is bent over her desk, sobbing. Marcus stands waiting. Professional but firm. Ms. Whitmore, he says quietly. It’s time to go.

She fumbles with her badge, drops it, pick it up with shaking hands, her office keys, her company phone, everything that identified her as branch manager. 6 years gone in 6 minutes. As Marcus escorts her toward the door, she tries one more time. Dr. Carter, please. I’m sorry. I didn’t understand. Regina doesn’t turn around. You understood perfectly.

You just didn’t think there would be consequences. The glass door closes behind Diane Whitmore. She’ll never work in banking again. Diane is halfway across the lobby when Robert Brooks bursts through the main entrance. He’s 46, usually composed, but right now he looks like he’s been running. His tie is loose.

His face is flushed. He scans the lobby, spots Regina, and walks directly to her. Ignore everyone else. Dr. Carter. He’s breathing hard. I got your message. I was at my daughter’s soccer game. I drove here as fast as I could. He glances at Diane, who’s frozen near the door with Marcus. Is it true? Everything you texted, every word.

Robert turns to Diane, his voice shakes with barely controlled fury. You told Dr. Regina Carter, our CEO, our founder, the woman who built this entire company, that she’s nobody. The remaining customers in the lobby pull out their phones. This is going to be everywhere by tonight. Diane can barely speak. I didn’t know.

She didn’t tell me. How was I supposed to? You weren’t supposed to know. Robert’s professionalism cracks. You were supposed to treat every customer with respect. That’s literally your job. Marcus clears his throat. He’s still standing next to Diane, but he turns slightly toward the gathering crowd. His voice carries authority from 30 years of police work.

For those who don’t know, he says, addressing the customers and employees. Dr. Regina Carter founded First Western Financial Holdings 12 years ago. She started with one branch in Seattle. She grew it to 50 branches across six states. She’s CEO of the parent company that owns this bank and she sits on the boards of Intel, Providence Health Systems, and Kaiser Permanente.

And he pauses, letting that sink in. She’s been featured in Forbes, Fortune, and the Wall Street Journal. She was Oregon Business Magazine’s executive of the year, two years running. Before she went into finance, she was a neurosurgeon at OSU. She has more power in one phone call than anyone in this building will have in their entire career.

The lobby is silent except for the classical music still playing overhead. The absurd normaly of it. Marcus looks at Diane and you told her she’s nobody. Dian’s legs give out. She sits down hard on the marble floor, her back against the wall. She’s still crying, but now it’s the kind of crying that comes from complete destruction.

Her career, her reputation, everything gone. Regina walks over to where Jamal is standing. He’s watching everything with wide eyes. She puts a hand on his shoulder. You asked me why I didn’t tell her who I was from the start, she says quietly, though others can hear. This is why. Because the janitor deserves the same respect as the CEO.

The teacher deserves the same respect as the board member. If service depends on knowing someone’s title, then it’s not service. It’s a performance. She looks at Robert Brooks. How long has Diane Whitmore been branch manager here? 6 years. And in those 6 years, how many discrimination complaints were filed against her? Robert’s jaw tightens.

He pulls out his phone, accesses something. According to HR records, seven formal complaints, all dismissed as personality conflicts or misunderstandings. Seven, Regina’s voice is cold. Pull up the demographic data on those complaints. Robert types. His face goes gray. All seven were from customers of color. Five black, two Latino. Ms.

Patterson steps forward. Dr. Carter, I filed two of those complaints. I’m one of three black employees at this branch. I told HR that Diane made customers uncomfortable, that she asked different questions depending on who walked through the door. They told me I was being oversensitive. Kevin joins her.

I sent an email to HR 3 months ago. I documented five incidents where Diane requested additional verification from black and Latino customers that she never asked from white customers. I never got a response. Carlos, the young teller, speaks up. Last month, she made a black woman cry. The woman had a PhD. She was a professor at Portland State.

Diane questioned her employment three times, asked to see her tax returns for a basic savings account. The woman filed a complaint. Nothing happened. Regina turns to Robert. Nothing happened. Seven complaints, clear patterns, and nothing happened. Robert looks like he wants to disappear. Dr. Carter, I we have policies. We have training. I don’t know how.

I know exactly how. Regina’s voice cuts through his excuses because I review the training completion records every quarter. Diane completed her annual anti-discrimination training in 14 minutes last year. The course is designed to take 90 minutes. She clicked through every module as fast as the system would allow.

She pulls up something on her phone, turns it toward Robert. The case study in module 3 describes exactly what she did today. Requesting non-standard documentation. questioning fund legitimacy without cause, using policy as a shield for discriminatory treatment. She passed the quiz with 100%. But she didn’t read it. She didn’t learn it, and nobody followed up.

The system failed at every level. Regina walks to where Diane is still sitting on the floor. She crouches down, meeting her eyes. You asked if I knew who you were. Diane’s voice is horsearo. You’re right. I would have treated you differently. I would have You would have given me the same treatment you gave that couple.

Regina gestures to where the young white couple opened their account earlier. 8 minutes. No questions. No extra documentation. Smiles and pleasantries. That’s what everyone deserves. Not just CEOs, not just white people. Everyone. She stands. I dressed casually today. I drove a regular car. I didn’t flash credentials because I wanted to see how my employees treat ordinary customers and now I know. Robert’s phone buzzes.

He looks at it then at Regina. Legal department wants to know how you’d like to proceed. They’re recommending immediate termination, formal investigation, and proactive outreach to any other affected customers. Agreed. Regina doesn’t hesitate. But I want more than that. I want a full audit of every branch.

I want customer service metrics broken down by demographics. I want to know how widespread this is. Yes, ma’am. Regina turns to Jamal. You still need a checking account. Kevin practically runs to his computer. I’ll open it right now. Premium account, all fees waved for 2 years. And on behalf of everyone here who isn’t, he glances at Diane.

like that. I’m so sorry. Regina nods. Thank you, Kevin. I saw you documenting everything. That took courage. While Kevin processes the account, Regina looks at the text message she sent earlier. Timestamp 11:02 a.m. to Robert Brooks. Discrimination incident. Downtown branch. Diane Whitmore. Standby. She sent it the moment Diane demanded the birthday money verification list.

That was 23 minutes ago. She gave Diane 23 minutes to correct the course. Multiple chances to stop, to reconsider, to treat them with basic dignity. Diane declined every single one. And now, sitting on the marble floor of the bank she used to manage, Diane Whitmore understands exactly what she’s lost. Not just a job, not just a career, her entire identity.

Because for six years, she was the branch manager. She had power. She had authority. She decided who belonged and who didn’t. And in 6 minutes, she discovered she’d been wielding that power over the one person who could take it all away. The woman she called nobody. The woman who is in fact everything. Two weeks later, Regina Carter sits at the head of a conference table in the first Western Financial Holdings headquarters in Seattle.

10 board members, the chief legal officer, Janet Woo from HR. Robert Brooks looked significantly more nervous than usual. On the screen behind Regina, a single statistic glows in white letters against a dark background. 31. 31 customers, Regina begins, her voice measured, received discriminatory treatment from Diane Whitmore over the past 18 months, not 6 years, just the last year and a half.

That’s how far back we could verify with certainty using transaction logs, security footage, and employee testimony. She clicks to the next slide, a graph showing demographic breakdown. Of those 31 customers, 23 were black, six were Latino, two were Middle Eastern, zero were white. She lets that sit for a moment. This wasn’t implicit bias.

This was a pattern. The legal officer, Martin Webb, interrupts. Dr. Carter, before we proceed, I need to state for the record that these findings are preliminary. And Martin, Regina’s voice is ice. We have video evidence, statistical analysis, 17 written testimonies from employees, 12 customer complaints that were dismissed. This isn’t preliminary.

This is a documented fact. She clicks again. Split screen video footage appears. On the left, Diane Whitmore greeting a white couple in their 40s, smiling, laughing at something the husband said. Processing their account in 8 minutes flat. No questions about employment. No requests for additional documentation.

On the right, Diane with a black woman in her 30s. No smile, arms crossed, 23 minutes of questioning. Three separate requests for additional paperwork. The woman leaves without opening an account. Same day, Regina says, same account type, same initial deposit amount, 2 hours apart. She plays another comparison. White man in his 20s wearing a hoodie and ripped jeans.

Opens a checking account in six minutes. Diane jokes with him about his university sweatshirt. Black teenager in a button-down shirt and khakis. Questioned for 18 minutes about the source of his funds, asked if his parents know he’s at the bank. Diane calls his employer to verify his paycheck before proceeding. The pattern, Regina continues, is consistent, documented, and indefensible.

Robert Brooks clears his throat. We’ve contacted all 31 customers. 27 have accepted our apology and restitution offer. Four are considering legal action independently. What’s the average settlement? A board member asks. $2,500 per customer plus fee wavers for 5 years. Total exposure $77,500. Janet Woo pulls up the spreadsheet.

That’s just direct restitution. It doesn’t include legal fees if any of the four proceed with lawsuits. Regina advances to the next slide. This one shows training completion records. Diane Whitmore completed mandatory anti-discrimination training four times in 6 years. Average completion time 16 minutes. The course is designed to take 90 minutes minimum.

She clicked through every module, answered the quiz questions using the review sheet visible on the screen, and collected her certificate. She clicks again. 73% of our branch managers complete training the same way. They’re checking a box, not learning, not changing. The room shifts uncomfortably. We have a systemic problem, Regina says flatly. Diane Whitmore is a symptom.

The disease is that we built a compliance system that allows people to pretend they’re complying. Martin Webb tries again. With all due respect, Dr. Carter, one branch manager’s behavior doesn’t necessarily indicate. Regina cuts him off with a single click. The screen now shows a map of all 50 First Western Financial Holdings branches.

Five of them are highlighted in red. Five branches, five different managers, all showing statistically significant disparities in how they treat customers of different races. She zooms in on the data. Branch 12 in Tacoma. Black customers wait an average of 14 minutes longer than white customers for the same services.

Branch 27 in Sacramento. Latino customers are three times more likely to have account applications delayed for additional review. Branch 8 in Boise. Middle Eastern customers are flagged for fraud screening at five times the rate of white customers with identical transaction patterns. The board is silent now.

We found this in two weeks of analysis. Regina continues. 2 weeks using data we already had. This has been happening for years and nobody looked. Janet Woo stands taking over the presentation. Dr. Carter asked us to examine not just individual complaints, but patterns across the entire organization. We analyzed 200,000 customer interactions from the past 3 years. The results are troubling.

She clicks through charts showing response times, approval rates, additional documentation requests, fraud flags, and service quality scores, all broken down by customer race. In every single metric, Janet says, customers of color receive measurably worse service than white customers. Sometimes it’s seconds, sometimes it’s minutes, sometimes it’s the difference between approval and denial, but it’s consistent across branches, across states, across our entire operation.

A board member, Patrician, speaks up. Are you saying our entire company is discriminatory? I’m saying, Regina responds, that we built systems without adequate oversight. We hired managers without proper screening. We implemented training that doesn’t train. And when employees reported problems, we dismissed them as personality conflicts.

She pulls up emails, internal HR communications, all marked confidential. Evelyn Patterson reported Diane Whitmore in March of last year. The HR response, customer service styles vary. No action needed. Kevin Morrison reported her in November. HR response, manager discretion is within policy. Closed. Carlos Mendoza reported her in February of this year. HR never responded at all.

Regina looks directly at Janet Woo. Why? Janet’s face is tight. Our HR team was understaffed. We prioritized legal liability over employee concerns. We had have a culture that protects managers over customers and frontline staff. And that ends today, Regina says. She advances to a new slide. Proposed reforms. The list is extensive.

Immediate actions. Terminate Diane Whitmore for cause already completed. Place four other managers on administrative leave pending investigation. Retain third-party firm to audit all branches for discriminatory patterns. Establish $500,000 fund for customer restitution and community outreach. Policy changes.

Mandatory bias testing before any promotion to management. Mystery shopper program with diverse participants. Quarterly visits to every branch. Realtime AI monitoring of transaction patterns to flag disparities immediately. Anonymous employee hotline with guaranteed investigation within 72 hours. Customer complaints escalate to executive level after single HR dismissal.

Training overhaul replace click-through modules with in-person workshops requiring demonstrated competency. Monthly case study reviews led by diversity consultants. Quarterly one-on-one assessments with random branch staff. Failure to pass results in immediate suspension and retraining. Accountability measures. Branch manager bonuses tied to equitable service metrics, not just profitability.

Public annual diversity report showing demographic breakdown of service quality. Board level equity and inclusion committee with authority to override executive decisions. Employee whistleblower protections with financial incentives for reporting discrimination. Patricia and Gwyn studies the list. This is aggressive.

The cost alone, the cost of doing nothing, Regina interrupts, is our reputation, our customer base, and potentially our banking license. The FDIC takes discrimination seriously. So does the Consumer Financial Protection Bureau. If they investigate us and find what we found, we don’t get to control the narrative.

Martin Webb looks pained. Dr. Carter, some of this might expose us to additional liability. If we acknowledge systemic issues, then we acknowledge them. Regina’s voice is final. I didn’t build this company to be the kind of institution that values legal protection over doing what’s right. We failed 31 customers, probably more.

We’re going to fix it. She clicks to the final slide. A photo of Jamal Carter sitting in the bank lobby two weeks ago trying not to cry while his mother gets called nobody. This is my son, Regina says quietly. He’s 16 years old. He got his first job. He wanted to open his first bank account and he learned that someone in authority could look at him and decide he’s suspicious, criminal, unwelcome based on nothing but what he looks like.

She lets the image stay on the screen. He learned that lesson at my bank in my company because I didn’t do enough to prevent it. She looks around the table. That stops now. The vote is unanimous. All reforms approved. After the meeting, Robert Brooks approaches Regina. Dr. Carter, I want to apologize. Diane reported to me.

I should have seen the pattern. You should have, Regina agrees. So should HR. So should I. We all failed. She pauses. But now we fix it. How long until the third party audit is complete? 6 weeks for a preliminary report. 3 months comprehensive. I want weekly updates. And Robert? She looks at him directly. You’re a good regional director, but you missed this.

Everyone in your position is going to receive additional training on identifying discrimination, including you. Yes, ma’am. Later that evening, Regina sits in her home office reviewing the employee testimonies. 17 people came forward once they knew it was safe. 17 people who’d seen something wrong and tried to report it.

One testimony stands out from Marcus Thompson, the security guard. I’m a black man who worked as a police officer for 30 years. I know what discrimination looks like. I saw Diane do it dozens of times. I documented what I could. I reported twice to branch management. Nothing happened. When Dr. Carter walked in that day, I recognized what was happening immediately.

Part of me was relieved that someone with actual power was finally experiencing what regular customers go through. Maybe now something would change. I hate that it took the CEO being discriminated against for anyone to care, but I’m grateful something is finally happening. Regina reads it three times. He’s right. It shouldn’t have taken the CEO experiencing discrimination for the system to respond, but it did.

And that’s the most damning evidence of all. The system was broken. Not because it lacked policies, but because it only enforced those policies when someone powerful enough to demand accountability was harmed. Everyone else could be ignored. Not anymore. Regina opens her laptop and begins drafting an email to all 50 branch managers.

The subject line, “Change is coming. Be ready.” In 2 weeks, the mystery shopper program launches. Real customers, diverse backgrounds, unannounced visits, testing whether the reforms are working or just more performance. This time there will be consequences. This time people are watching. This time it’s not just about Diane Whitmore.

It’s about whether an entire institution can choose to be better than it was. 3 months after that Saturday morning, the transformation is visible. The downtown Portland branch has a new manager, Sandra Kim, 39, Korean-American, previously assistant manager at the Beaverton location. She greets every customer the same way, warm, professional, no assumptions.

On a Tuesday afternoon, a young black man in a hoodie walks in. He’s nervous. First time opening an account. Sandra processes everything in 9 minutes. Asks about his job with genuine interest. welcomes him to the bank. He leaves smiling. This is what it should have been all along. Ms. Patterson is still there.

So is Kevin, now in management training. Carlos got promoted to senior teller. The people who reported discrimination and were ignored are now the ones helping rebuild trust. But what about Diane Whitmore? She doesn’t work in banking anymore. Can’t. Her termination was coded fired for cause discrimination. It’s a public record.

Every background check shows it. Her banking license was revoked after an ethics review. The state banking commission found her actions violated professional conduct standards. She tried to fight it. Hired a lawyer. The lawyer dropped her case after reviewing the evidence. 17 witness statements, security footage, statistical analysis showing a pattern across 31 customers.

There was nothing to defend. She applied for jobs outside banking, a retail management position. They Googled her name, found news articles. Bank manager fired after calling CEO nobody. The story went viral. 6 million views. She didn’t get the job. Her husband filed for divorce 4 weeks after the incident. He told his lawyer he couldn’t be married to someone like that.

Their kids changed their last name to his. She moved out of Portland. Some people say she’s in Idaho now, working at a call center, barely making rent. Others say she left the state entirely. Nobody knows for sure. Nobody cares because Diane Whitmore doesn’t matter anymore. The system that enabled her does. First Western Financial Holdings released its first annual equity in banking report in September.

The data is public, transparent, uncomfortable. The report shows that before the reforms, black customers waited an average of 4.2 minutes longer than white customers for service. Now it’s 0.3 minutes. Latino customers were denied accounts at 2.7 times the rate of white customers with identical financial profiles. Now it’s 1.1 times.

Still not equal, but closer. The mystery shopper program runs continuously. Diverse participants visit branches unannounced, testing for discriminatory treatment. Two managers were fired in the first month, not for dramatic incidents like Dian’s, just for patterns, for asking different questions, for subtle discrimination that would have been invisible before.

The anonymous hotline receives 40 calls per month. Every single one is investigated within 72 hours. Five employees have received financial awards for reporting discrimination. The message is clear. Speaking up is rewarded, not punished. Branch manager bonuses are now tied to equity metrics. If your branch shows disparities in service quality across racial groups, you don’t get paid.

Simple as that. Suddenly, every manager cares deeply about equal treatment. The training is real now. In-person workshops, role-playing scenarios. A black facilitator asks white managers what they’d do if a young black man walked in with cash. They have to answer out loud, have to confront their assumptions, have to prove they understand. The program isn’t perfect.

Some branches still show disparities. Some managers still harbor biases. But now there’s accountability, measurement, consequences. The 31 customers who were discriminated against all received restitution. Most accepted the bank’s apology. Three pursued additional legal action and received confidential settlements.

One customer, a black woman who’d been made to feel like a criminal for depositing her PhD stipend, used her settlement to start a nonprofit helping people of color navigate financial discrimination. Regina Carter chairs the newly formed equity and inclusion committee. She reviews data quarterly. She visits branches unannounced.

She sits in on training sessions. She reads every hotline complaint personally. She doesn’t trust the system to fix itself. So, she watches it constantly because she knows what happens when nobody’s watching. She experienced it firsthand in her own bank with her own son. At the downtown Portland branch, there’s a new plaque on the wall near the entrance. It wasn’t there 3 months ago.

It reads, “We serve everyone with equal dignity and respect. If you experience discrimination, report it. We will listen.” Below it, a QR code links directly to the anonymous hotline. Sandra Kim insisted on putting it there. She says it’s a promise to customers, to employees, to everyone who walks through those doors.

Some promises are kept, some aren’t. This one is being tested every single day. So far, it’s holding. 6 months later, Regina and Jamal sit at their kitchen table. His debit card, the premium account from that day, sits between them. worn now, used regularly, normal. Do you think things actually changed? Jamal asks, or did people just get better at hiding it? Regina doesn’t give him comfortable lies.

Both. Some changed because they had to, some because they wanted to, some just perform compliance better now. That’s why we measure, watch, hold people accountable. It’s exhausting. It is. But the alternative is worse. The alternative is what happened to us happening to someone without a CEO’s phone number.

Someone who just walks away. Jamal traces his cards. Edge. I still think about what she said. That we’re nobody. I know. Does it get easier? No. But you get stronger. You remember that someone calling you nobody says everything about them, nothing about you. She pauses and you use whatever power you have to make sure they can’t do it again.

That’s that’s the real lesson. Not revenge, not dramatic justice, accountability, systems, follow through. Diane Whitmore’s story isn’t about one bad person getting punished. It’s about a system that let her discriminate for 6 years, that dismissed complaints, that protected managers over customers, that confused checking boxes with actual change.

It’s about what happens when someone with power decides to use it. But here’s the uncomfortable truth. Regina Carter had power. She could make one phone call and end a career. What about everyone else? The customers who experienced identical discrimination but didn’t have the CEO’s number. The employees who reported problems and were ignored, they deserved the same protection, the same accountability, the same justice.

They didn’t get it until someone powerful enough to demand it experienced it firsthand. That’s what we can’t forget. Systems don’t change from moral inspiration. They change when staying the same costs too much. when the CEO gets discriminated against, when the story goes viral, when reform becomes necessary. So, here’s your question.

Have you witnessed someone abuse power based on assumptions about who belongs at a bank, store, school, anywhere? Did you speak up, document it, report it, or stay silent because it wasn’t happening to you? The system changed for Regina Carter because she had power. What about everyone else? If you’ve experienced discrimination, document everything.

Names, dates, exact words, screenshots, record if legal, file formal complaints. Get written responses. If you witness discrimination, don’t look away. Be a witness. Offer statements. Your voice might tip the scale. If you hold power like Diane did, ask yourself what assumptions you’re making, who you’re treating differently, what biases you’re bringing to decisions.

The difference between Diane and accountability wasn’t that she was uniquely terrible. It was that she finally discriminated against someone who could enforce consequences. That shouldn’t be the requirement for justice. But until it isn’t, we document, report, speak up, hold systems accountable. Like this video if you believe accountability matters.

Subscribe for stories about systems that change. Share with someone who needs to see it. Justice isn’t one person getting fired. It’s building systems where the next teenager doesn’t need his CEO mother just to open a checking account. It’s making dignity the default, not the exception. See you next time. >> At Black Voices Uncut, we don’t polish away the pain or water down the message.

We tell it like it is because the truth deserves nothing less. If today’s story spoke to you, click like, join the conversation in the comments, and subscribe so you’ll be here for the next Uncut Voice.

Disclaimer : This content may be created by AI for entertainment purposes. Any resemblance to real persons, events, or places is coincidental.